Market Commentary: The Iran Conflict and Portfolios Built to Weather Storms

The Situation: What Has Happened

On 28 February 2026, the United States and Israel launched coordinated military strikes against Iran — code-named Operation Epic Fury by the US and Operation Roaring Lion by Israel. Targets included nuclear facilities, military installations, and key regime figures, including Iran's Supreme Leader Ali Khamenei. President Trump has indicated that operations are expected to continue for approximately four to five weeks.

Iran has responded with retaliatory missile strikes, attacks on US assets in the Gulf region, and — most consequentially for energy markets — has warned that the Strait of Hormuz would be closed to tanker traffic. This narrow waterway carries approximately 20% of the world's oil and liquefied natural gas supply, making it one of the most strategically critical passages controlling global oil and gas trade.

The conflict has also drawn in Hezbollah in Lebanon, with alleged drone attacks on the US Embassy in Riyadh, and triggered strikes on energy infrastructure across Gulf states. As of the time of writing, the situation remains fluid and evolving.

Immediate Market Reaction: Measured, Not Panicked

The strikes sent shock-waves through global markets — oil prices surged and equities experienced a sharp sell-off in the opening hours of trading. But the initial market reaction proved short-lived as investors quickly began assessing the probable scope and duration of the conflict:

• Oil prices surged 6–9% on the first day of trading, with Brent crude rising to approximately $78 per barrel — an 8-month high — on fears of sustained Strait of Hormuz disruption.

• Gold rallied approximately 2%, briefly reclaiming $5,400 per troy ounce as investors sought safe-haven assets.

• The US dollar strengthened, with the dollar index gaining as capital flowed toward perceived safety.

• US stocks recovered intraday losses swiftly — the S&P 500 closed essentially flat, the Dow fell less than 75 points after being down nearly 600 points at the open.

• European and Asian markets fell more sharply, with the pan-European STOXX 600 slipping 1.61% and Japan's Nikkei dropping 1.35%.

• Defense stocks rallied — Northrop Grumman and RTX both rallying strongly.

• Airlines sank on fuel costs concerns and disruptions over Europe and the Middle East.

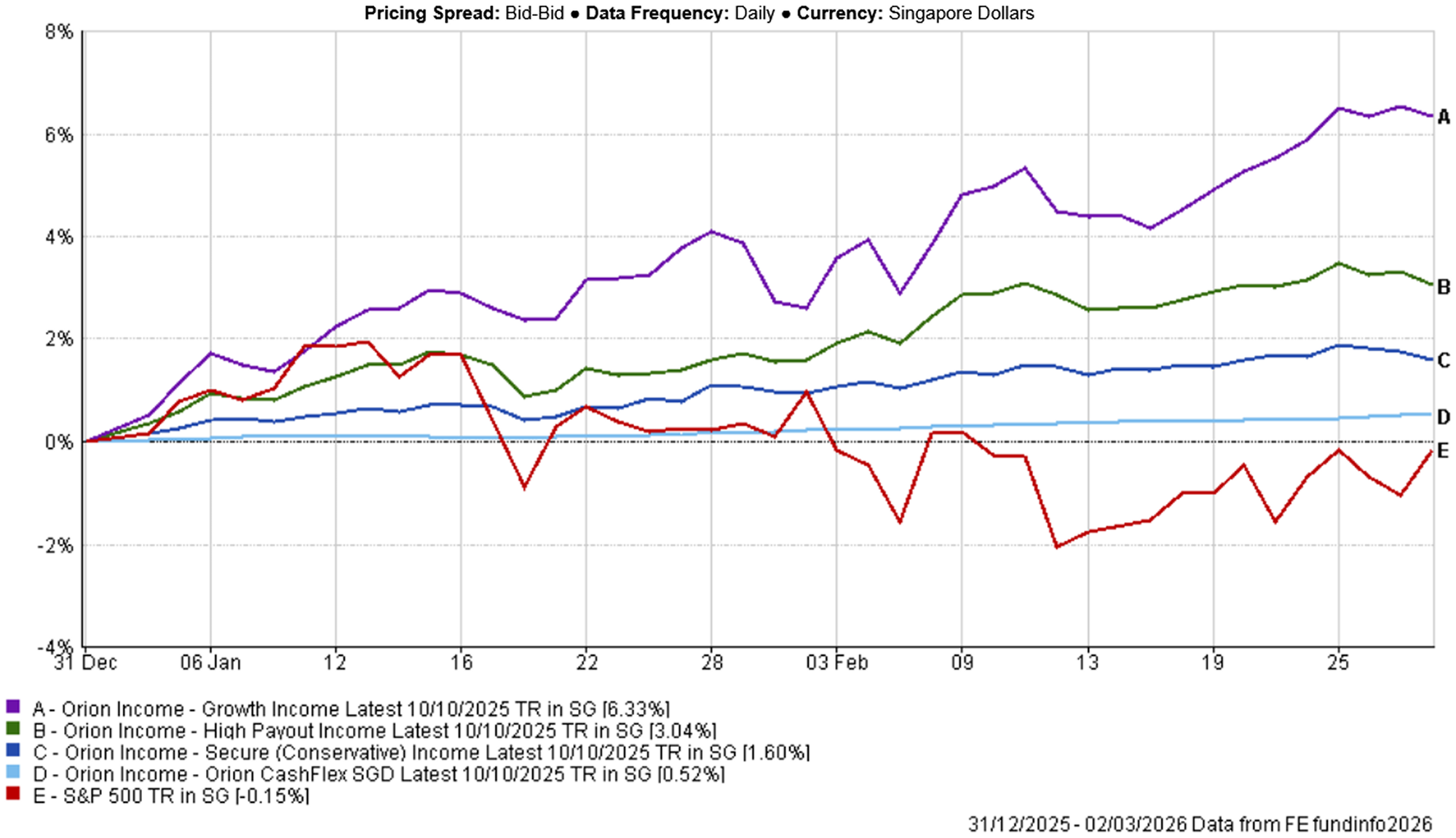

Your Portfolios: Positioned for Exactly This Environment

Our investment strategy has long been anchored in defensive, income-generating assets — globally diversified across sectors, with a clear focus on steady income generation and capital preservation. Periods of geopolitical uncertainty are precisely when this approach demonstrates its resilience. Here is why your portfolios are well-positioned:

- Profitable, Income-Generating Assets Provide a Cushion

Unlike growth-oriented or speculative assets that trade on future earnings expectations, income-generating investments — such as dividend-paying equities, property and infrastructure assets, and fixed income — derive their value from current cash flows. During turbulent periods, these cash flows continue to arrive regardless of daily market movements, providing both stability and return.

When sentiment turns negative, investors historically shift out of higher-risk, higher-volatility positions and into precisely the kind of stable, cash-flowing assets that form the core of your portfolios. This shift can actively benefit defensive holdings during periods of uncertainty. - History Is Clear: Geopolitical Shocks Are Temporary

Market history provides strong reassurance. According to Morgan Stanley strategists, the S&P 500 has averaged gains of 2%, 6%, and 8% in the one, six, and twelve months following major geopolitical risk events — from data going back to the Korean War in 1950 and the 1956 Suez Crisis. The consistent pattern across more than 70 years of history is that markets absorb geopolitical shocks, recover, and then resume their long-term trajectory.

The current conflict echoes previous Middle East confrontations. When Israel struck Iran in June 2025, Brent crude posted a sharp single-day gain — only to fall sharply once a ceasefire was reached. Markets have seen these situations before, and they know how to find their footing. - Energy Markets Have Meaningful Buffers

While the Strait of Hormuz disruption is genuinely significant, energy market analysts have highlighted several factors that mitigate the severity:

• Global oil markets entered this conflict from a position of strong supply, with countries such as China holding strategic stockpiles both onshore and in floating storage.

• Shortly after the conflict began, OPEC announced an intended production increase of 206,000 barrels per day from April 2026, helping to partially allay fears of any disrupted oil supply.

• Saudi Arabia has contingency pipelines (the East-West pipeline via the Red Sea) that can route oil flows around the Strait.

• Iran's own oil exports — approximately 1.6 million barrels per day, mostly to China — represent a relatively contained portion of global supply.

Analysts at Evercore ISI suggest that a scenario where oil stabilises around $80 per barrel with a relatively short conflict would result in only limited economic impact. The more disruptive scenario — oil above $100 per barrel — would require a significantly prolonged conflict and sustained infrastructure damage, which markets are not currently pricing as the base case.

What This Means for Investors: Stay the Course

Some short-term volatility is inevitable and should be expected. Markets dislike uncertainty, and there is currently plenty of it. Paper losses may appear on statements over the coming weeks, and it is natural to feel unsettled when headlines are alarming.

However, selling into fear is one of the most consistent ways investors lock-in losses and destroy long-term wealth. The evidence spanning decades and multiple major conflicts is clear: those who remain invested through geopolitical disruptions consistently outperform those who attempt to time their way in and out of markets.

The defensive positioning of your portfolios means that any losses incurred during this period are likely to be:

• Contained — because income-generating assets are less sensitive to sentiment-driven sell-offs than growth or speculative positions.

• Temporary — because history shows markets recover from geopolitical shocks, and defensive assets are typically among the first to stabilise.

• Partially beneficial — because rising oil prices benefit certain holdings within diversified income portfolios, including energy-related equities and infrastructure assets, and flight-to-safety can benefit other investments within the portfolios.

Key Risks We Are Monitoring

While our base case remains constructive, we are closely watching the following variables:

• Duration of the conflict — Trump has indicated a 4 to 5 week timeline. A conflict extending beyond this significantly changes the calculus.

• Oil price trajectory — if Brent crude approaches or exceeds $100 per barrel, the inflationary and growth implications may be more serious.

• Strait of Hormuz reopening — a credible path to securing this critical waterway would likely trigger a sharp positive market reaction.

• Regional escalation — involvement of additional state actors or attacks on major Gulf oil infrastructure represent the primary upside risk to oil prices.

• Federal Reserve response — higher oil prices may delay anticipated rate cuts, which could create headwinds for rate-sensitive assets.

Our Commitment

We are monitoring the situation closely and will continue to communicate if conditions change materially. Our investment strategy — built on durable, income-generating assets with strong fundamentals — was not constructed for fair-weather markets alone. It was constructed precisely for times like this.

The noise will be loud, the headlines will be alarming. As in past corrections, we expect volatility to be contained and temporary — and the portfolios remain well-placed to preserve capital, generate sustainable income, and achieve their long-term objectives despite the near-term uncertainty.

If you have questions or concerns, please reach out to your financial consultant. Or Contact us to to help you navigate this with clarity and confidence.

Disclaimer

References: https://www.cnn.com/2026/03/02/investing/oil-us-stock-market-iran

Evercore ISI has been ranked No. 1 among all firms for top-ranked analysts on a weighted basis in the Extel All-America Equity Research survey for four consecutive years as of 2025 — the industry's most authoritative analyst ranking.

Krishna Guha is Evercore ISI's Vice Chairman and a former senior official at the US Federal Reserve. His credibility on geopolitical and macro market calls comes directly from his policy background — he spent years at the Fed before moving to the private sector, giving him a perspective that pure equity analysts do not have.